Why CHAGEE chose Singapore and Cayman Islands for its IPO structure

In its recent IPO filing with the U.S. Securities and Exchange Commission, CHAGEE (through its Cayman-incorporated entity) revealed a familiar but carefully considered cross-border corporate structure: using Singapore as a holding platform for its China business, and Cayman Islands as the ultimate listing vehicle.

SINGAPORE 新加坡OFFSHORE 离岸

Adept CS

4/28/20254 min read

Why CHAGEE Chose Singapore and Cayman Islands for Its IPO Structuring?

In its recent IPO filing (referencing its F-1 Form submitted) with the U.S. Securities and Exchange Commission, CHAGEE (through its Cayman-incorporated entity) revealed a familiar but carefully considered cross-border corporate structure: using business incorporation in Singapore as a holding platform for its China business, and Cayman Islands as the ultimate listing vehicle. This strategy — increasingly common among China-based companies seeking global capital — offers distinct legal, operational, and regulatory advantages.

Below, we explore why CHAGEE structured its IPO this way, and specifically why Singapore Corporate Structure plays a critical intermediary role between China and the listing vehicle in Cayman.

1. Why Cayman Islands for the Listing Vehicle?

The Cayman Islands is a jurisdiction of choice for many U.S.-listed Chinese companies, including giants like Alibaba and JD.com. Key reasons include

Familiarity for Global Investors: Cayman-incorporated entities are widely accepted by U.S. and international investors. They are well understood in terms of corporate governance and shareholder rights.

Flexible Corporate Law: Cayman law provides flexibility in share structures (such as dual-class shares), corporate governance, and shareholder protections — features attractive for founders and pre-IPO investors.

Tax Neutrality: Cayman does not impose corporate income taxes, capital gains taxes, or withholding taxes, minimizing tax leakage at the listing entity level.

Streamlined Regulatory Framework: Setting up and maintaining Cayman entities is relatively straightforward and cost-effective compared to many other jurisdictions.

Thus, for CHAGEE, Cayman Islands as the topco offered a trusted, neutral base to raise funds internationally — particularly through a U.S. IPO.

2. Why Singapore as the Intermediate Holding Company?

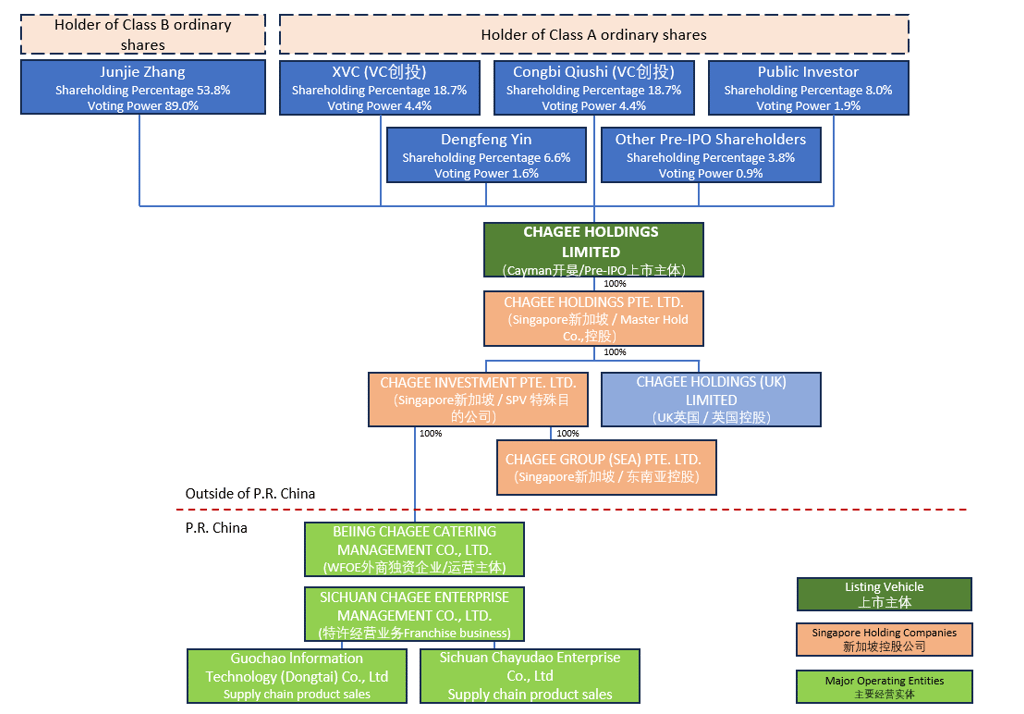

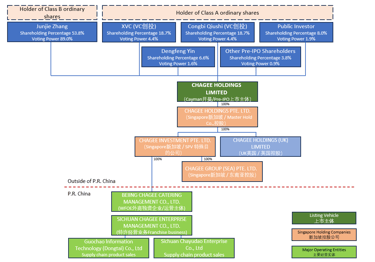

What’s particularly notable in CHAGEE’s structure through the setup of Singapore Company to hold the Chinese operating entities (the Wholly Foreign-Owned Enterprises, or WFOEs). Here’s why Singapore makes strategic sense:

a. Political and Legal Stability

Singapore provides strong rule of law, political neutrality, and an independent judiciary, making it one of the most attractive jurisdictions globally for holding investments, especially in sensitive sectors like food and beverage (where CHAGEE operates).

b. Investment Protection Treaties

Singapore has an extensive network of bilateral investment treaties (BITs) and free trade agreements (FTAs), including treaties with China. This gives additional protection to investments made by Singapore-incorporated companies in China, reducing sovereign risk.

c. Favorable Tax Regime

Low corporate tax rate (currently capped at 17%).

No capital gains tax and no withholding tax on dividends paid to foreign shareholders under certain conditions.

Singapore also offers tax incentives for regional holding companies and exemptions on foreign-sourced dividends under its foreign-sourced income exemption (FSIE) regime.

For CHAGEE, using a Singapore intermediary could allow tax-efficient repatriation of profits from China to investors abroad.

d. Economic Substance Compliance

In today’s world of anti-tax avoidance rules (BEPS, OECD initiatives, etc.), simply using a low-tax jurisdiction like Cayman without real operations can trigger scrutiny.

By using incorporating a Singapore vehicle — where actual management and operational activities (such as IP ownership, finance functions, or regional management) can be legitimately based — CHAGEE can demonstrate substance in its structure.

e. Easier Future Expansion

Singapore serves as a gateway to Southeast Asia. Holding the China business through Singapore gives CHAGEE a natural platform for future regional expansion into ASEAN markets without major restructuring. Financial services in Singapore are exceptionally robust, making the city-state a prime hub for companies seeking to expand across borders.

3. Why Not Hold China Operations Directly Under Cayman?

Direct ownership of the China WFOE by the Cayman entity is theoretically possible, but:

It could raise concerns under China’s outbound investment rules.

It would expose the Cayman entity directly to China’s regulatory jurisdiction and tax system.

Having an intermediary like Singapore mitigates direct exposure and adds a layer of flexibility and protection.

Thus, CHAGEE’s use of Singapore Holding Company as the intermediary is a strategic move to balance control, protection, tax efficiency, and future scalability.

Conclusion

The IPO structure of CHAGEE — Cayman Islands for the public listing vehicle, and Singapore holding company setup as an intermediate holding, and China as the operations base — is not accidental. It reflects decades of learned best practices among China-focused companies going global.

Singapore, in particular, plays a critical strategic role: it not only protects CHAGEE’s China investments but also optimizes tax efficiency, demonstrates real operational substance, and provides a strong foundation for regional growth.

As more Chinese consumer brands like CHAGEE look outward for global capital and expansion, Singapore’s role as a trusted holding jurisdiction will likely become even more important in the years ahead.

This publication is provided for general information purposes only and is not intended to cover every aspect of the topics with which it deals. It does not constitute legal, tax, or accounting advice. Readers should not rely solely on this content for making decisions without consulting a qualified professional. Reading our articles does not create an attorney-client relationship between the reader and our firm.

While we strive for accuracy, laws and regulations change frequently, our articles may contain links to external websites or resources. We do not endorse or guarantee the accuracy of such content. We make no representations, warranties or guarantees, whether express or implied, that the content in the publication is accurate, complete or up to date. Use the information at your own risk.

Before taking any action based on our articles, consult a qualified attorney, tax advisor, or accountant pertaining to your unique situation. Always seek legal advice to ensure compliance with local regulations and ethical standards.

Adept Corporate Services (ACS) is a leading corporate service provider, offering comprehensive business solutions, including entity formation, corporate secretarial compliance, bank account opening (including offshore entities), corporate accounting, fund administration, tax compliance, MAS & SFC licensing & Compliance outsourcing, work visa applications, and payroll services.

Singapore| Malaysia | China | Hong Kong SAR | USA | British Virgin Islands | Cayman Islands

新加坡 | 马来西亚 | 中国 | 香港特别行政区 | 美国 | 维京群岛 | 开曼群岛

©2021-2026 Adept Corporate Services | All Rights Reserved