The Sunsetting of Red Chips? Navigating HKEX & CSRC Listing Rules 2026

With the 2026 HKEX update, the "Red Chip" era is evolving. Learn the key differences between Red Chip and H-Share structures and the new CSRC filing requirements for Chinese companies.

CORPORATE SECRETARIAL COMPLIANCEHONG KONG 香港TAX PLANNING 税务筹划

Adept

3/30/20264 min read

For decades, the Red Chip structure was the "gold standard" for Chinese firms tapping global capital. However, as of 2026, the shift toward H-share direct listings is accelerating. Driven by CSRC "post-filing" mandates and HKEX's push for transparency, mainland companies are moving from "internationalized offshore entities" to "regulated mainland extensions."

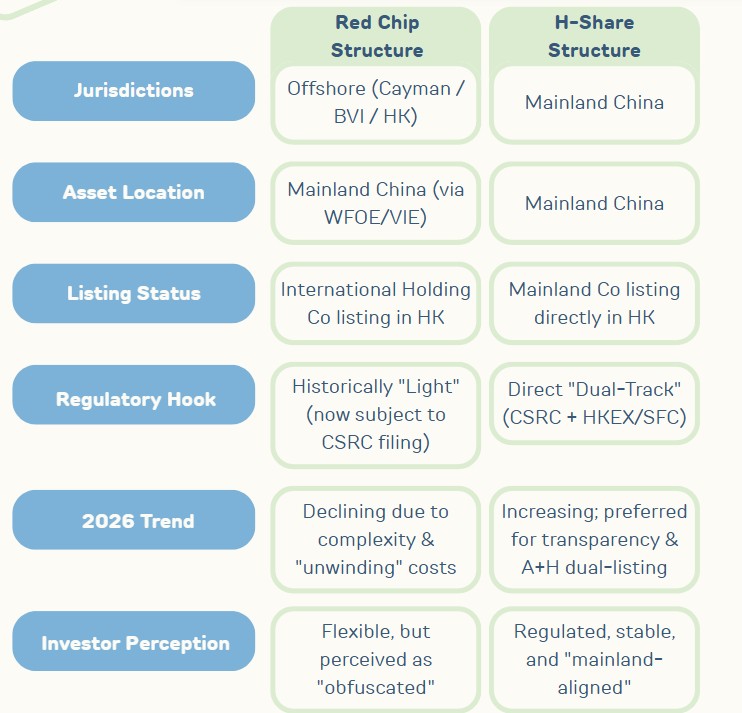

1. What is a Red Chip? (The Definition) Red Chip vs H-share 2026

In the world of overseas listing for Chinese companies, the term "Red Chip" is steeped in both history and symbolism. Coined in the early 1990s, the name combines "Blue Chip" (high-quality companies) with "Red" to represent the Chinese government’s involvement.

Technically, a Red Chip is a company that satisfies three main criteria:

Incorporation: It is incorporated outside of Mainland China (typically in Hong Kong, Bermuda, or the Cayman Islands).

Ownership: It is substantially controlled (directly or indirectly) by Mainland Chinese state-owned entities (central, provincial, or municipal governments) although founded by Chinese entrepreneurs.

Operations: The majority of its revenue and assets are derived from Mainland China.

The Distinction: A red-chip structure is not limited to Chinese SOEs. It has evolved into a widely used offshore listing framework adopted by both state-owned and private Chinese enterprises seeking access to international capital markets.” Today, it commonly includes private Chinese companies using offshore holding structures for overseas listings.

2. How is it Used? (The Strategic Playbook)

The Red Chip structure was the most used structure for Chinese companies who are looking to list ourside of China. It was used as a bridge:

Access to Global Capital: By listing in Hong Kong through an offshore entity, these companies could attract foreign institutional investors who were more comfortable with Hong Kong’s legal system and the British Common Law framework.

Operational Flexibility: The offshore structure allowed for easier mergers and acquisitions, more flexible dividend policies, and the use of complex share structures like "weighted voting rights" (dual-class shares).

Currency Advantages: It allowed companies to raise funds in HKD or USD, facilitating international expansion and providing a hedge against RMB fluctuations.

Famous examples include heavyweights like Tencent, Meituan, China Mobile and CNOOC, which used this route to become global giants.

3. The Current Clampdown: Why the Shift?

The "playbook" is being rewritten - China Securities Regulatory Commission (CSRC)is now discouraging new Hong Kong IPO listing applications from companies using the Red Chip structure.

Key reasons for the clampdown include:

* Regulatory Transparency: The China Securities Regulatory Commission (CSRC) is pushing for "Mainland incorporation." By having companies incorporate within China, the regulator has more direct oversight over their financial health and data security.

* Curbing Capital Flight: There are concerns that offshore structures make it easier for capital to leave the country in ways that are harder to track.

* Streamlining Compliance: Following a massive boom in Hong Kong IPOs, regulators are worried about "deal quality." They are now asking companies to dismantle their offshore structures (unwinding the Red Chip) and re-organize as Mainland entities before listing.

How about Variable Interest Entity (VIE) structures?

Since 2023, the CSRC (China Securities Regulatory Commission) has tightened the "Red Chip/VIE" route. Previously, these offshore companies operated in a "gray area" of Chinese law. Now, any company with major operations in China—whether they are a Red Chip (SOE) or a P-Chip (Private)—must file for approval with the CSRC before listing in Hong Kong or the US.

4. The Future Look: A New Era of "Onshore-First"

The future for the classic Red Chip looks increasingly restrictive. We are likely entering a transition period where:

* Dismantling Structures: Many Hong Kong IPO listing candidates will face delays (some estimated at 6 months or more) as they scramble to "unwind" their offshore holdings to meet new CSRC preferences.

* The Rise of H-Shares: We will likely see a surge in H-share listings (Mainland-incorporated) as the preferred route, despite the more rigid regulatory requirements regarding capital outflows.

* Impact on Foreign VC/PE: For private equity and venture capital firms (including many based in Singapore), this shift makes "exits" more complicated. Investing in a Mainland-incorporated company involves stricter foreign exchange controls when it comes time to sell shares and repatriate funds.

* Hong Kong’s Role: While Hong Kong remains the primary gateway for Chinese capital, the nature of the companies listing there is changing from "internationalized offshore entities" to "strictly regulated mainland extensions."

5. So what is H-share listing?

H-shares represent a direct listing structure where a company incorporated in mainland China issues shares to foreign investors on the Hong Kong Stock Exchange.

Since March 2023, China has shifted from a "pre-approval" to a "post-filing" system for overseas listings, streamlining the process . The journey now involves a dual-track approval process with both mainland and Hong Kong regulators.

CSRC Filing (China): The company must file with the China Securities Regulatory Commission (CSRC) within three working days after submitting its listing application (the "A1") to the HKEX listing.

HKEX & SFC Review (Hong Kong): The HKEX and SFC conduct a joint review. The review period can be as short as 30 business days for large, highly compliant A-share companies, and typically up to 40 business days for others

Closing Thought for Clients

For businesses and investors in Asia, these changes signal a move toward "total oversight" by Beijing. While the Hong Kong IPO listing market remains vibrant, the era of using offshore "Red Chip" structures to bypass mainland rigidity is drawing to a close. Staying compliant now requires a much deeper understanding of the CSRC’s filing regimes and a readiness to embrace mainland corporate structures from the outset.

At Adept, we don't just process filings; we navigate the human and regulatory complexities of cross-border restructuring. Whether you are unwinding an old structure or starting fresh, we ensure your team stays focused on growth while we handle the compliance.

This publication is provided for general information purposes only and is not intended to cover every aspect of the topics with which it deals. It does not constitute legal, tax, or accounting advice. Readers should not rely solely on this content for making decisions without consulting a qualified professional. Reading our articles does not create an attorney-client relationship between the reader and our firm.

While we strive for accuracy, laws and regulations change frequently, our articles may contain links to external websites or resources. We do not endorse or guarantee the accuracy of such content. We make no representations, warranties or guarantees, whether express or implied, that the content in the publication is accurate, complete or up to date. Use the information at your own risk.

Before taking any action based on our articles, consult a qualified attorney, tax advisor, or accountant pertaining to your unique situation. Always seek legal advice to ensure compliance with local regulations and ethical standards.

Adept Corporate Services (ACS) is a leading corporate service provider, offering comprehensive business solutions, including entity formation, corporate secretarial compliance, bank account opening (including offshore entities), corporate accounting, fund administration, tax compliance, MAS & SFC licensing & Compliance outsourcing, work visa applications, and payroll services.

Singapore| Malaysia | China | Hong Kong SAR | USA | British Virgin Islands | Cayman Islands

新加坡 | 马来西亚 | 中国 | 香港特别行政区 | 美国 | 维京群岛 | 开曼群岛

©2021-2026 Adept Corporate Services | All Rights Reserved