Tax Exemption Schemes for Companies in Singapore

Singapore is a business-friendly country, and the government introduces policies to help foster entrepreneurship and business growth. One of the ways this is through the introduction of two tax exemption schemes which are applicable to most companies.

Adept CS

4/28/20253 min read

Singapore is a business-friendly country, and the government introduces policies to help foster entrepreneurship and business growth. One of the ways this is through the introduction of two tax exemption schemes which are applicable to most companies.

Understanding Singapore's Tax Exemption Schemes for Companies

Singapore offers two primary tax exemption schemes to encourage business growth and entrepreneurship: the Tax Exemption Scheme (TES) for New Start-Up Companies and the Partial Tax Exemption (PTE) Scheme. Both aim to reduce the tax burden on companies, the first cater to new businesses, while the other is for operating companies.

Although Singapore’s prevailing corporate tax rate is 17% (one of the lowest in the Asia Pacific region), through these tax exemption schemes, the effective tax rate on the first S$200,000 of Singapore companies’ taxable profits can be reduce to less than 5%, if certain conditions are met. This makes Singapore an attractive location for inspiring entrepreneurs and seasoned businessmen alike to setup companies for their next commercial venture.

We will cover more details on the tax exemption schemes in the sections below. If you like to know more about the tax exemption schemes, please feel free to reach out to us at [adept@adept-cs.com] and our tax specialist will reach out to you.

1. Tax Exemption Scheme (TES) for New Start-Up Companies

This tax exemption scheme is to reduce the tax burden of new start-up companies in Singapore so they can reinvest their profits to grow and build their build their capabilities. The tax exemption is applicable for the for first 3 consecutive years of assessment of the start-up company only. From the fourth year of assessment onwards, companies can enjoy the partial tax exemption scheme which we will cover in the next section

Eligibility Criteria:

Incorporation: The company must be incorporated in Singapore.

Tax Residency: The company must be a tax resident of Singapore for the assessment year.

Shareholding: The company must have no more than 20 individual shareholders throughout the basis period for that year, with at least one individual shareholder holding a minimum of 10% of the issued ordinary shares.

Key Features:

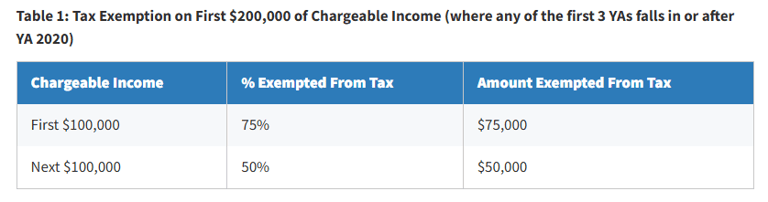

Period: The first 3 consecutive years of assessment falls in or after YA 2020

First $100,000: 75% exemption on the first $100,000 of normal chargeable income.

Next $100,000: 50% exemption on the next $100,000 of normal chargeable income.

Exceptions:

Generally, the TES does not apply to:

Companies that undertake property development for sale, investment or both.

Investment holding companies.

2. Partial Tax Exemption (PTE) Scheme

Companies that do not qualify for the TES can benefit from the PTE Scheme.

Key Features:

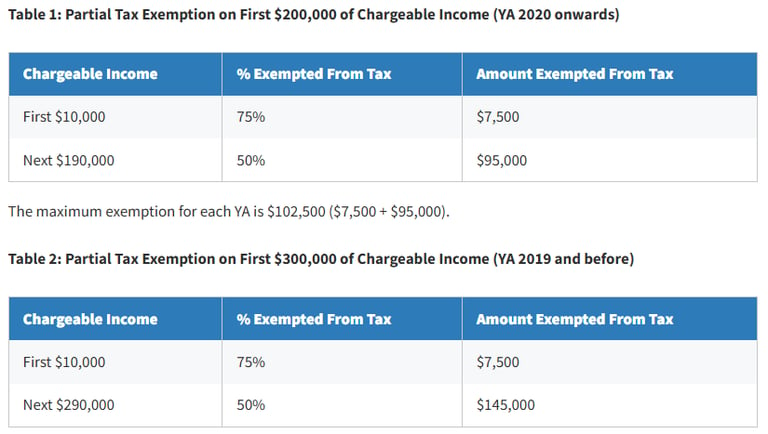

First $10,000: 75% exemption on the first $10,000 of normal chargeable income.

Next $190,000: 50% exemption on the next $190,000 of normal chargeable income.

Conclusion

Both the TES and PTE schemes are designed to support businesses growth by reducing their tax liabilities. Companies should assess their eligibility for these schemes to optimize their tax positions. Please note that the IRAS takes a serious view of companies that are setup to abuse the tax exemption schemes (i.e. not for genuine commercial reasons). This might result in severe penalties, fines and even jail terms. For detailed information, you can reach out to us at adept@adept-cs.com to speak to our tax specialist who can help advice on your eligibility for these schemes.

This publication is provided for general information purposes only and is not intended to cover every aspect of the topics with which it deals. It does not constitute legal, tax, or accounting advice. Readers should not rely solely on this content for making decisions without consulting a qualified professional. Reading our articles does not create an attorney-client relationship between the reader and our firm.

While we strive for accuracy, laws and regulations change frequently, our articles may contain links to external websites or resources. We do not endorse or guarantee the accuracy of such content. We make no representations, warranties or guarantees, whether express or implied, that the content in the publication is accurate, complete or up to date. Use the information at your own risk.

Before taking any action based on our articles, consult a qualified attorney, tax advisor, or accountant pertaining to your unique situation. Always seek legal advice to ensure compliance with local regulations and ethical standards.

Adept Corporate Services (ACS) is a leading corporate service provider, offering comprehensive business solutions, including entity formation, corporate secretarial compliance, bank account opening (including offshore entities), corporate accounting, fund administration, tax compliance, MAS & SFC licensing & Compliance outsourcing, work visa applications, and payroll services.

Singapore| Malaysia | China | Hong Kong SAR | USA | British Virgin Islands | Cayman Islands

新加坡 | 马来西亚 | 中国 | 香港特别行政区 | 美国 | 维京群岛 | 开曼群岛

©2021-2026 Adept Corporate Services | All Rights Reserved