Dormant Company in Singapore: ACRA definition vs IRAS definition & Tax Filing Waivers

In Singapore, ACRA and IRAS have distinct interpretations on the definition of a dormant company Singapore.

Adept Cs

5/12/20254 min read

In Singapore, ACRA and IRAS have distinct interpretations on the definition of a dormant company Singapore. Below is an overview of both:

Dormant Company Definition from ACRA (Accounting and Corporate Regulatory Authority)

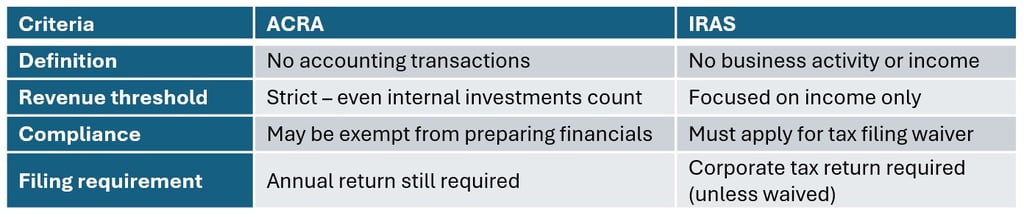

According to ACRA, a company is classified as dormant if it has “no accounting transactions” throughout a financial year. A dormant company in Singapore is a registered company that is not receiving any form of income or is actively trading.

What disqualifies a company from being dormant:

· Payment or receipt exceeding the nominal sum of S$5,000

· Employing staff

· Selling and buying goods and services

· Buying or leasing property

· Issuing dividends to shareholders

· Paying directors’ salaries

· Receiving dividend payments or managing investments

· Investments in subsidiaries

Transactions of a company arising from any of the following are to be disregarded:

(a) the taking of shares in the company by a subscriber to the constitution pursuant to an undertaking of the subscriber in the constitution;

(b) the appointment of a secretary of the company;

(c) the appointment of an auditor;

(d) the maintenance of a registered office;

(e) the keeping of registers and books;

(f) the payment of any fee or charge (including any fee, penalty or interest for late payment) payable under any written law;

- the payment of any composition amount payable under Section 409B of the Companies Act or any other written law;

- the payment or receipt by the company of such nominal sum not exceeding such amount as may be prescribed (prescribed value: not exceeding S$5,000);

(g) such other matter as may be prescribed.

ACRA permits dormant exempt private companies (individual shareholder) in Singapore to be relieved from the obligation of preparing financial statements, provided they fulfil specific criteria.

Can a dormant company own property in Singapore?

From a tax perspective, a company that did not carry out any business activities and had no income is considered as a dormant company. As such, if a company holds a property but did not rental it out or do any business with the property and had no income from this property, it is possible to argue that the company is dormant for the period. Generally, if a company is considered dormant for ACRA purposes, we can take a deeper look to determine if it meet the condition for a dormant company for tax purposes as stated above.

Do I need to file Form C-S for a dormant company?

A dormant company must file a Form C-S every year with the Singapore tax office, IRAS.

How do I apply for a tax return waiver with IRAS?

To apply for a waiver to file Form C-S, this can be done via the IRAS website, and you will have to prepare the tax returns for the advance Years of Assessment, financial statements and tax computations (where applicable) to submit to the IRAS too.

What is the difference between ACRA and IRAS dormant status in Singapore?

This publication is provided for general information purposes only and is not intended to cover every aspect of the topics with which it deals. It does not constitute legal, tax, or accounting advice. Readers should not rely solely on this content for making decisions without consulting a qualified professional. Reading our articles does not create an attorney-client relationship between the reader and our firm.

While we strive for accuracy, laws and regulations change frequently, our articles may contain links to external websites or resources. We do not endorse or guarantee the accuracy of such content. We make no representations, warranties or guarantees, whether express or implied, that the content in the publication is accurate, complete or up to date. Use the information at your own risk.

Before taking any action based on our articles, consult a qualified attorney, tax advisor, or accountant pertaining to your unique situation. Always seek legal advice to ensure compliance with local regulations and ethical standards.

Dormant company requirements of IRAS (Inland Revenue Authority of Singapore)

Definition of Dormant Company:

IRAS defines a company as dormant if it does not engage in any business activities and has no income for the entire financial period. The company will be regarded as a dormant company for tax purposes for the year of assessment (e.g. Company setup on 1 January 2024 but did not carry on a business and had no income for the whole year of 2024 - regarded as dormant for YA 2025).

Do dormant companies need to file taxes in Singapore?

Although a dormant company did not have any revenue, it is still required to file a corporate income tax return by 30 November every year (however, exempt from filing ECI), unless the company had applied and granted for a waiver to file Form C-S / Form C-S (Lite) / Form C by the IRAS.

If you think your company might qualify as a dormant company for corporate tax purposes, feel free to reach out to us and we can help to determine if your company meet the dormant conditions to qualify for wavier to file tax return.

Read More: Key Factors to Consider While Choosing a Registered Filing Agent in Singapore

Adept Corporate Services (ACS) is a leading corporate service provider, offering comprehensive business solutions, including entity formation, corporate secretarial compliance, bank account opening (including offshore entities), corporate accounting, fund administration, tax compliance, MAS & SFC licensing & Compliance outsourcing, work visa applications, and payroll services.

Singapore| Malaysia | China | Hong Kong SAR | USA | British Virgin Islands | Cayman Islands

新加坡 | 马来西亚 | 中国 | 香港特别行政区 | 美国 | 维京群岛 | 开曼群岛

©2021-2026 Adept Corporate Services | All Rights Reserved